News Release from American Clean Power Association (ACP)

Wind Industry Profile of

NEW REPORTS: 2022 Marks Third-Highest Year for U.S. Utility-Scale Solar, Wind, and Storage Installations

- 11% growth in the now nearly 140 gigawatt (GW) development pipeline reflects promise of new federal policies, while historically low Q4 2022 and Q1 2023 installations demonstrate lingering headwinds

- Total clean power installations declined in 2022 for the first time in five years

- Texas added over 9 GW of clean energy in 2022, the most in the U.S., while Iowa and South Dakota each generated over 50% of their electricity from clean power

- Energy storage had a record year with 4 GW and 12 GWh installed, an 80% capacity increase

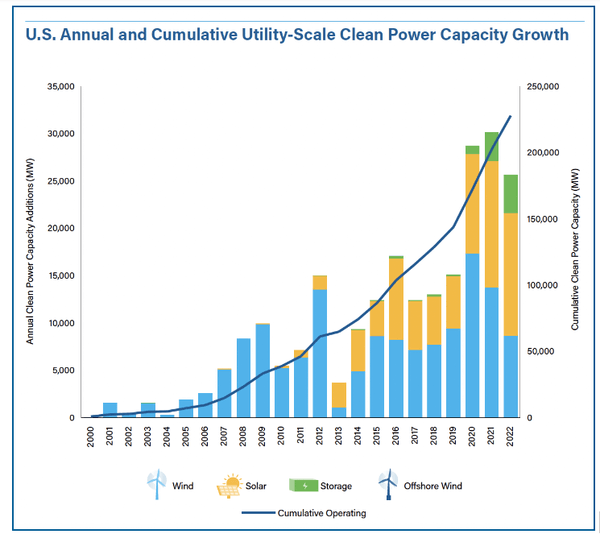

Chart: U.S. Annual and Cumulative Utility-Scale Clean Power Capacity Growth – Clean Power Annual Market Report | 2022

Today, the American Clean Power Association (ACP) released its comprehensive Clean Power Annual Market Report for 2022 and its Clean Power Quarterly Market Report for Q1 2023, finding that combined U.S. wind, utility solar, and energy storage capacity had the third-largest year on record in 2022 with over 25 gigawatts (GW) of new clean power installed. However, a decline in deployment volume from the previous two years, combined with a historically low Q1 2023, underscore the continued headwinds facing the industry.

After historic clean energy incentives were signed into law in August 2022, clean power has seen record levels of announced activity, with the development pipeline swelling to nearly 140 GW by the end of Q1 2023 – 11% above where it was at the same point last year. However, it is too early to see this activity translate into installations, which have slowed for the first time since 2017.

“The clean energy revolution is underway,” said ACP CEO Jason Grumet. “We have the technology, financial capital and workforce to power our economy with clean, affordable and secure energy. There is broad bipartisan support for American energy innovation. But the clean energy transition will not succeed unless Congress and Governors enable the siting and construction of new energy facilities and support the build out of transmission that is required to bring clean power to the people.”

By the end of 2022, nearly 228 GW of clean energy was online, with 4 GW more added in Q1 2023. These resources provide 15% of the nation’s electricity and deliver enough electricity to power the equivalent of over 62 million households. Clean power dominated new power capacity additions in 2022, comprising nearly 80% of all new grid additions.

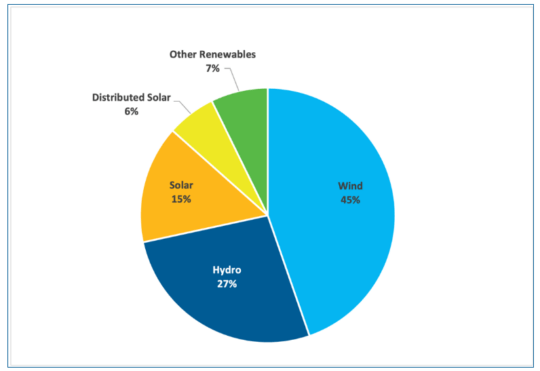

Chart: U.S. Renewable Generation by Technology – Clean Power Annual Market Report | 2022

Texas added twice as much clean energy capacity as any other state in 2022 (over 9 GW), maintaining its status as the state with the most operating clean power capacity (nearly 55 GW). Iowa and South Dakota each generated over half of their electricity from clean power last year.

Energy storage witnessed a record year in 2022 with 4 GW and 12 GWh commissioned, representing an 80% increase in total operating storage capacity.?Hybrid project installations in 2022 were 60% higher than in 2021, setting a new record in the hybrid space at nearly 6 GW of installations.

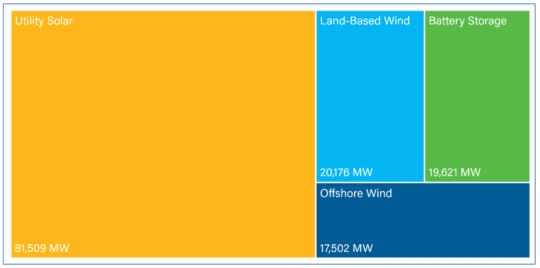

In the nearly 140 GW development pipeline, solar accounts for 59% of all clean power capacity. Land-based wind accounts for 15% of the pipeline, battery storage represents 14%, and offshore wind claims the remaining 13%.

Chart: 139 GW Development Pipeline by Technology – Clean Power Quarterly Market Report | Q1 2023

Headwinds & Delays

However, the year’s progress was not enough to continue the annual growth trajectory of U.S. clean power, with the industry seeing a decline in combined installation volume for the first time in five years and the lowest Q1 (2023) in three years.

Contributing to the slowdown in installations were delays in 2022 that affected over 50 GW of projects in late-stage development, with a total of 63.3 GW – equivalent to powering nearly 7 million homes – experiencing delays by the end of Q1 2023. On average, these projects face delays of six months or longer, depriving ratepayers of clean, affordable electricity.

Project delays are primarily due to unclear permitting timelines, trade policy uncertainty, transmission shortages, difficulties sourcing solar panels, unresolved IRA implementation, and interconnection queue challenges (with over 1,741 GW waiting in queues at the end of 2022).

These challenges must be addressed to unlock the full potential of the nearly 140 GW of clean energy in the development pipeline.

Key Highlights – Overall

- Third-Largest Year: 25.5 GW of new clean power was commissioned in 2022, making it the third-largest year on record and bringing the total amount of American clean power online by year’s end to nearly 228 GW.

- Leading Source of New Power: Clean power represented 79% of all new capacity added in 2022.

- Powering More of America: By the end of Q1 2023, wind and solar provided 232 GW of clean energy, over 15% of the country’s electricity and equivalent to powering over 62 million homes.

- Net-Zero Progress: Maintaining last year’s project installation volume would provide only 30% of what is needed to reach a net-zero grid by 2035.

- Significant Delays: By the end of 2022, 53 GW of projects were experiencing delays due to ongoing regulatory, supply chain and interconnection challenges, contributing to a 15% decline in deployment volume from 2021. 63.3 GW of clean power was delayed by end of Q1 2023.

- Development Pipeline: 139 GW of clean energy projects were under development at the end of Q1 2023.

- Storage Soars: In 2022, energy storage witnessed a record year with 4 GW and 12 GWh commissioned, representing an 80% increase in total operating storage capacity.

- Growing Workforce & Investment: The clean power industry employs 443,000 workers and invested $35 billion in capital investment in 2022.

- United States of Clean Energy: Clean power is red, white, and blue with projects or manufacturing facilities in 93% of Congressional districts. Projects can be found in all 50 states.

- Booming Manufacturing: There are 550 U.S. manufacturing facilities dedicated to producing components and parts for wind, solar, and storage projects in the clean power industry – and since the passage of the Inflation Reduction Act (IRA), 47 new clean energy manufacturing facilities or expansions have been announced, bringing more than 18,000 new American jobs.

Key Highlights – Q1 2023

- Lowest Q1 Since 2020: Q1 2023 saw a 36% drop in clean power installations (4,079 MW) compared to Q1 2022.

- 95 project phases were commissioned across 27 states, with Florida and Texas leading.

- Sector Snapshot: Solar led the quarter (2,200 MW), followed by wind (1,418 MW) and battery storage (461 MW).

- Delays: Regulatory challenges led to significant project delays, especially in the solar sector, with 7.3 GW of clean power capacity expected online in Q1 delayed, for a total of 63.5 GW of clean power delayed by end of Q1.

- 90% of Q1 delayed capacity expected to come online later in 2023.

- Pipeline: The development pipeline grew 11% from Q1 2022 to 139 GW, dominated by solar at 59%.

- PPAs: New Power Purchase Agreement (PPA) announcements fell by 24% to 3.8 GW, with corporate buyers leading at 63%.

The Clean Power Market Reports for 2022 and Q1 2023 are comprehensive overviews of the U.S. wind, utility solar, and energy storage markets, containing in-depth analysis of key industry statistics, trends, and rankings. The 180-page annual report and the Q1 2023 report are available exclusively to ACP members.

A public website with interactive data from the 2022 annual report can be viewed here.

- Source:

- ACP

- Author:

- Press Office

- Link:

- cleanpower.org/...

- Keywords:

- ACP, report, wind, solar, utility scale, storage, battery, installation, clean poer, gigawatts, USA

All news from American Clean Power Association (ACP)

news in archive

Related News