News Release from Rystad Energy

Wind Industry Profile of

Iberia: A new European energy powerhouse emerges

With reliable gas supply from North Africa, lower power prices compared to the rest of Europe, and a renewable energy pipeline that stands out on the continent, Spain and Portugal have the potential to evolve into a new European energy powerhouse, according to Rystad Energy research.

Spain became Europe’s third-largest power exporter in the first three quarters of 2022, behind only Sweden and Germany. The key reasons for this were a large shortfall in power generation in France, from where Spain normally imports power, in addition to the Iberian price cap on gas-fired power generation. This lowered Spain and Portugal’s electricity prices compared to France for large parts of this year and in turn made power exports even more competitive.

The Iberian market has proven to be resilient during the energy crisis as it does not rely on Russian gas. With limited domestic gas supplies, Iberia receives most of its gas through pipelines from Algeria and through long-term import contracts for liquefied natural gas (LNG). Algerian gas exports to Spain are estimated to reach 14.6 billion cubic meters (Bcm) in 2022 and the regasification capacity of Spain and Portugal together represents about 68 Bcm per annum, which is one-third of Europe’s total regasification capacity. Sufficient regasification capacity enables more gas sources to reach the Iberian gas market. The region imported about 28 Bcm for the first nine months of 2022, surpassing last year’s total imports, which leads us to expect that total LNG imports to the Iberian Peninsula will climb to about 39 Bcm this year.

The region is expected to see strong growth in overall power generation this year as well as sustained growth in the years ahead, driven mainly by the massive expansion of renewables. The share of renewables in the Iberian power mix is expected to rise from 48% in 2021 to 64% in 2025 and 79% in 2030, putting the region at the forefront of the European energy transition.

“Through a combination of investment, geography and policy, Spain and Portugal have managed to avoid or reduce the impact of the European energy crisis. Rystad Energy is focusing on the Iberian market because the fundamentals point to it becoming a regionally significant energy-industrial hub”, says Carlos Torres Diaz, head of power at Rystad Energy.

Image: Rystad Energy

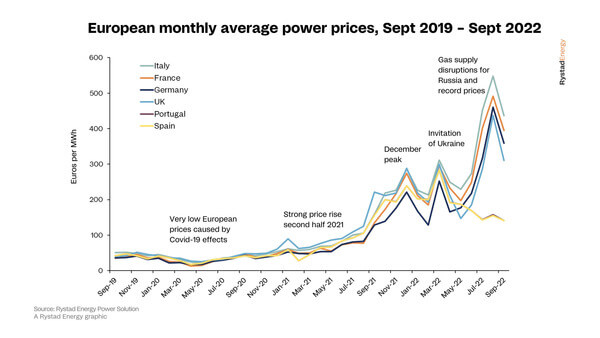

The below figure shows the development of European power prices over the past three years. Until 2021, Iberian power prices were closely coupled with other European countries. Both the rise and volatility in power prices have been extreme since the second half of 2021, and until June 2022 Iberian prices were still close to the other countries. However, after the price cap was introduced in June 2022, the effect has been clear – in August, power prices in Spain averaged €155 ($152) per megawatt-hour (MWh), while the rest of the selected countries had prices two or three times higher.

Image: Rystad Energy

Iberia could be expected to have a less painful ride ahead through the energy crisis compared to its European peers, as the Iberian market expects power prices to stay far below the levels in, for example, France and Germany. Power traded for the coming months and years is at a much lower level in Spain. In the short term, prices will continue to be suppressed by the price cap on gas-fired electricity, so for the coming winter prices are not directly comparable. But even with long-term contracts – such as yearly contracts for 2024 and 2025 – Spanish power is expected to be much cheaper than in France and Germany. The Spanish 2024 yearly contract is currently trading at €113 per MWh, more than half the price of the French equivalent at €270 per MWh. This points to a structural advantage in Iberia, the way the market currently sees it, and a bright future for power generation in the region.

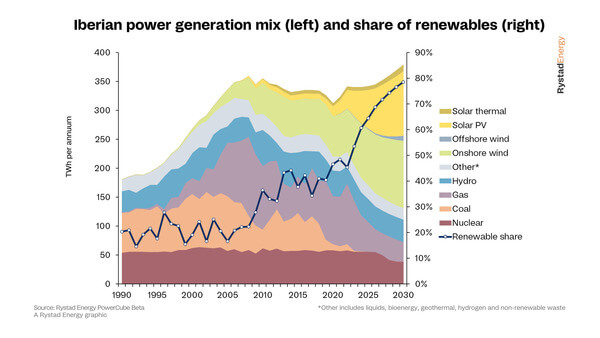

The relatively cheap forward power prices are supported by strong underlying fundamentals. France has massive challenges with its large nuclear fleet and few other alternatives for power generation, while Germany will struggle for years to come to reduce its reliance on Russian gas, cut its share of coal in the power mix, and deal with full nuclear shutdowns. Iberia has none of these problems. Spain has no reliance on Russian gas, and the Iberian Peninsula has by far the largest regasification capacity in Europe, in addition to North African imports – which together could make the region a European gas hub. Nuclear power will continue to deliver clean and cheap electricity for another decade, and both Spain and Portugal are close to completing, or have already completed, their coal phaseout plans. Also, the fundamentals for renewables are positive, with strong growth expected. Total Iberian power generation from 1990 until today, as well as Rystad Energy’s base case forecast for the power mix, is shown in the below figure.

Images: Rystad Energy

Leader of renewable energy in Europe in 2030

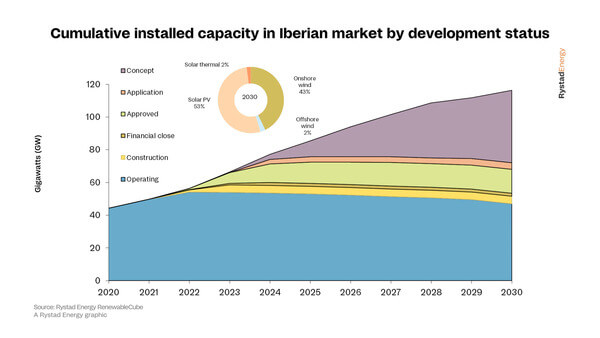

As a pioneer in the European wind industry, Spain is currently the second-largest generator of renewable power in Europe. The Iberian Peninsula currently has more than 50 gigawatts (GW) of installed capacity, with over 60% coming from onshore wind – and it will not end there. The region has ambitious plans, and with the National Integrated Energy & Climate Plan, Spain aims to source 74% of its power from renewables by 2030. Solar PV installations have climbed rapidly in recent years, and this is expected to further accelerate. If all goes as planned, solar PV installations will catch up with onshore wind installations and make up more than half of the region’s renewable energy by 2030.

In Portugal, offshore wind is headed for a bright future as the government announced last month it will boost the country’s offshore wind target from 6 GW to 10 GW by 2030, which will most likely be awarded through auctions. Portugal is also on track to host the world’s first subsidy-free commercial floating offshore wind project with BayWa’s permit application for a 600-megawatt (MW) floating offshore wind project off the Portuguese coast.

Iberia to the rescue for European gas consumers

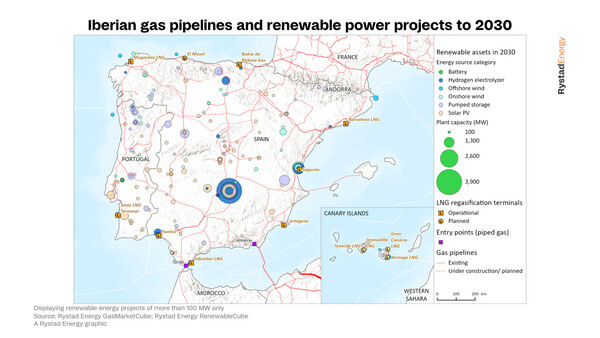

The Iberian Peninsula consumes about 40 Bcm of gas per year and is equipped with infrastructure to receive both African pipeline gas and international LNG cargoes.

Iberia has not been unaffected by the energy crisis and surging prices that have hit European gas hubs and the global LNG market. The peninsula has not, however, had the same need as many other European countries to replace Russian gas, find new supplies, and scramble to boost LNG import capacity. In fact, unutilized Spanish regasification capacity has provided valuable support as Spain has been able to send more gas to alleviate continental Europe’s gas deficit.

Spain has already transported about 1.7 Bcm of natural gas during the first 10 months of 2022 via the existing two pipelines – the Irun-Biriatou gas pipeline and Larrau–Villar de Arnedo gas pipeline – at the border of Spain and France. This is four times the volume exported in the same period last year. To make use of more of its excess LNG importing capacity and export more gas to Northwest Europe, Spain would technically be able to deliver more gas via the existing pipeline capacity to France, which connects the Iberian Peninsula with the market in Continental Europe.

Meanwhile, it was revealed late last week that the MidCat gas-pipeline project, which would have run from Iberia to Central Europe and was expected to have annual export capacity of 8 Bcm, has officially been abandoned and will be replaced by a new project called BarMar. The new project is a subsea gas pipeline from Barcelona in Spain to Marseille in France that will gradually replace fossil fuel in the system with renewable gases such as green hydrogen. The prime ministers of Portugal, Spain and France will meet in December to discuss financing of the project. This is not the first time hydrogen has been placed on the agenda for exporting Iberia’s renewable potential to help Europe wean itself off natural gas. Another corridor for green hydrogen trade is being planned by Cepsa between Algeciras in Spain and Rotterdam in the Netherlands, while Shell plans a hydrogen supply chain between Sines in Portugal and Rotterdam, to name just two potential projects.Iberia is well positioned to compete with – or even replace – Northern Europe’s existing energy industrial hub as sectors in Spain and Portugal can call on abundant sunshine, strong winds and mature gas infrastructure as well as a wealth of industry and managerial expertise. With reliable gas supply from North Africa, lower power prices compared to the rest of Europe and a renewable energy pipeline that stands out on the continent, Spain and Portugal have the potential to evolve into a new European energy powerhouse, according to Rystad Energy research.

For the first three quarters of 2022, the country became Europe’s third-largest power exporter, behind only Sweden and Germany. The key factors driving this includes a large shortfall in power generation in France, from where Spain normally imports power, in addition to the Iberian price cap on gas-fired power generation. This lowered Spain and Portugal’s electricity prices compared to France for large parts of this year and in turn made power exports even more competitive.

The Iberian market has proven to be resilient during the energy crisis as it does not rely on Russian gas. While having limited domestic gas supplies, Iberia receives most of its gas through pipelines from Algeria and through long-term LNG import contracts. Algerian gas exports to Spain are estimated to reach 14.6 Bcm in 2022 and the regasification capacity of Spain and Portugal together represents about 68 Bcma, which is one-third of the total European regasification capacity. Sufficient regasification capacity enables more gas sources to reach the Iberian gas market. The region imported about 28 Bcm for the first nine months of 2022, surpassing the total imports in 2021, which leads us to expect that total LNG imports to the Iberian Peninsula will increase to about 39 Bcm in 2022.

The region is expected to see strong growth in overall power generation in 2022, but also sustained growth going forward, driven mainly by the massive expansion of renewables. The share of renewable is expected to grow from 48% in 2021 to 64% in 2025 and 79% in 2030, putting the region at the forefront of the European energy transition.

- Source:

- Rystad Energy

- Author:

- Press Office

- Link:

- www.rystadenergy.com/...

- Keywords:

- Rystad Energy, Iberia, Spain, Portugal, renewable energy, Europe, gas, pipeline, power, electricity prices, LNG

All news from Rystad Energy

news in archive

Related News