News Release from Global Wind Energy Council

Wind Industry Profile of

Wind Turbine Suppliers see record year for deliveries despite supply chain and market pressures

Wind turbine suppliers supplied a new record amount of volume in 2022, according to GWEC’s annual Supply Side Data. According to the report, 30 wind turbine manufacturers installed 104.7 GW of new wind power capacity in 2021 despite continuing disruptions caused by the COVID-19 pandemic and increasing pressure from commodity price increases and logistical problems.

While turbine manufacturers delivered a record-breaking amount of projects in 2021 record-breaking deliveries, companies have shown worsening financial results due to an ultra-competitive price environment, higher external costs and continuing bottlenecks which are preventing a faster expansion in wind energy.

According to the International Energy Agency (IEA) the world needs to be adding around 390 GW of energy from wind generation by 2030 to keep the world on track to limit warming to 1.5°C. GWEC’s Global Wind Report 2022 found installations need to quadruple by 2030 to keep the world on course to reach that figure. These numbers can only be achieved with support for a market that delivers clean energy, clean jobs and works in fossil-fuel-free financial markets.

Ben Backwell, CEO of GWEC, said: “This new record in installations is a testimony to the key role which wind energy is playing in delivering the energy transition and protecting people and economies from high energy prices caused by fossil fuel volatility.

“However, as the UN Secretary General pointed out yesterday, governments need to urgently take action to kick start a much faster transition to renewables and remove barriers to deployment and investment, including cutting red tape and bureaucracy, fast-tracking grid investments and ensuring that markets adequately remunerate green energy instead of subsidising fossil fuels.

“The fact that wind turbine manufacturers are struggling to make a profit does not put the world in a strong position to scale up investment and reach the right level of installations – 390GW per year – that we will need to reach by the end of this decade.”

The Data

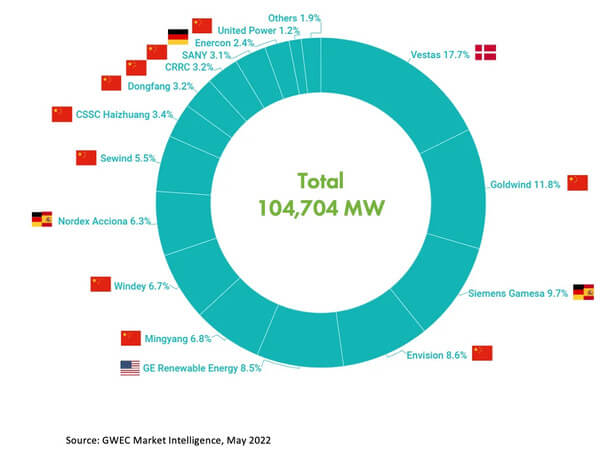

29,234 wind turbines were installed worldwide by 30 wind turbine manufacturers in 2021, of which 18 are from Asia Pacific and 9 from Europe.

Vestas enjoyed a record year to remain the number one turbine supplier, making 17.7% of the new installations. Chinese company Goldwind followed in second with 11.8%, holding its position from 2020, while Siemens Gamesa also had a record year with a 9.7% global market share, moving it up two positions to third place in 2021. Another Chinese company, Envision, is fourth with 8.65% of 2021’s market. GE Renewable Energy rounds out the top five with 8.55% of the market.

Top 15 wind turbine suppliers in annual global market in 2021 (Image: GWEC)

Vestas and Siemens Gamesa both enjoyed record years, with both companies leading the way in geographic diversification, with 37 and 32 countries delivered to, respectively. GE supplied 22 markets in 2021, while Goldwind and Envision only reached seven and three markets, respectively.

The upward trend in wind turbine rating and rotor diameter continues from last year. The average rated capacity of new turbines installed in 2021 surpassed the milestone of 3,500 kW while the rotor with the size greater than 140m accounted for more than 58% of the new installations. This is primarily due to the wind industry having a record year in new installations for offshore wind, while larger onshore wind turbines were installed in China after its onshore wind market entered the grid-parity era from 2021.

Top offshore wind turbine suppliers’ annual installed capacity 2021 (Image: GWEC)

Medium-speed wind turbines continue to gain popularity, the data shows, with its global market share increasing to 9.7 per cent in 2021, a 3.6 per cent rise relative to 2020. Mingyang and Vestas remain the key drivers in this turbine drive train solution with Goldwind, the world’s number one supplier of direct drive wind turbines, and Sewind, China’s leading offshore wind turbine supplier, both installed their commercial medium-speed turbines in 2021 for the very first time.

The double-fed induction generator (DFIG) remains the mainstream solution in 2021 with 50% of the market share, followed by direct drive permanent magnet generator (DD PMG), squirrel cage induction generator (SCIG,) and medium-speed PMG.

Feng Zhao, Head of Strategy and Market Intelligence of GWEC, said: “More than 100 GW wind power capacity was mechanically installed in 2021, making it the best year in global wind history and demonstrating the incredible resilience of the wind industry and global supply chain. The number of turbine suppliers dropped from 35 in 2020 to 30 in 2021, showing further market consolidation on the supply side, but the top six wind turbine OEMs lost 3% market share in 2021 as Tier 2 and 3 Chinese turbine OEMs gained more market share during the installation rush in China.

“Out of the global top 15 wind turbine suppliers in 2021, ten come from China, but only two Chinese make the top 5, a repeat of last year’s Top 15.

“Thanks for an astounding level of offshore wind growth at home driven by the feed-in tariff cut-off, however, Chinese suppliers dominated the offshore wind rankings last year with Siemens Gamesa and Vestas dropping out of the top 3 for the very first time. 2021 also saw the volume of exported Chinese turbines nearly tripled compared with 2020, but the Chinese OEMs’ market share outside China remains small,” he added.

The full report is available at GWEC’s Market Intelligence website: https://gwec.net/market-intelligence/

A note on the data:

The Global Wind Market Development – Supply Side Data 2021 represents a detailed account of wind turbines mechanically installed globally from all active suppliers over the past year – crucially this does not consider whether the turbines are grid-connected and commissioned.

The final report includes more than 30 tables and figures charting the evolution of global wind power markets on the supply side. This is the sister report to GWEC’s Global Wind Report 2022, which covers the global wind market status, based on annual grid-connected capacity.

Combining the two reports provides a powerful tool for our members to understand the global wind market development from both demand and supply sides.

- Source:

- GWEC

- Author:

- Press Office

- Link:

- gwec.net/...

- Keywords:

- GWEC; supply, data, report, record, logistics, pandemic, GW, 2021, installation, prices, costs, fossil, energy transition

All news from Global Wind Energy Council

news in archive

Related News