News Release from Wood Mackenzie Ltd

Wind Industry Profile of

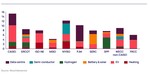

A global 261 GW wind portfolio hints at offshore wind evolution

With growth and ongoing consolidation as the backdrop, three other key trends are shaping offshore wind asset development and ownership.

- First, leading European players are pursuing higher returns by breaking into emerging markets while Chinese companies command a large and growing domestic pipeline.

- Second, the pool of offshore wind investors is being reshaped and expanded

- Third, the data reveals the rise of bidding consortiums in tenders and alliances among offshore companies.

Ambitious European companies are looking to emerging markets for partnerships and acquisition of pipelines and even companies to position themselves for future growth. Consequently, we saw a spike in offshore asset transactions in 2018 of 19.5GW – 69% of which came from emerging markets, such as United States, Taiwan, Poland and Ireland.

Emerging markets with maturing regulatory frameworks are the most appealing, though activity can begin well before the ink has dried on the page. Offshore wind developers are demonstrating a willingness to invest a significant amount of money to break into new markets, both by acquiring pipelines or companies. Both are on the table in some cases, as with Orsted’s acquisition of US offshore wind company Deepwater Wind.

While European players currently dominate the pursuit of new wind opportunities in the offshore wind industry globally, only one European company has secured a pipeline in China. Chinese state-owned companies have a corner on the huge domestic 84GW Chinese pipeline. The level of market consolidation is such that three out of the five largest offshore wind development portfolios are developed by Chinese companies.

Second, the pool of investors expands as institutional investors, APAC conglomerates and oil and gas majors are increasingly flocking to offshore assets. The growing investment appetite is fueled by a better understand construction and development risks from institutional investors combined with oil and gas majors and APAC conglomerates eagerness to break into the offshore wind industry. This trend is also apparent in US lease auctions, where both Shell and Equinor have secured capacity in two of the past three auctions.

The final set of trends in offshore wind ownership is the rise of tenders as well as the rise of alliances and bidding consortiums.

As the majority of demand moves into tenders and competition increases, analysts are seeing an increasing use of bidding consortiums in these tenders. In fact, almost 90% of companies participating in tenders in 2019 are expected to participate through bidding consortiums.

Moreover, alliances are increasingly being used by developers to break into, or fortify their position, in new markets – in 2018 alone, 15 alliances were formed

“New business models such as entering into alliances and forming ‘bidding consortiums’ is here to stay,” said Rolf Kragelund, Director of Global Offshore Wind at Wood Mackenzie.

- Source:

- Wood Mackenzie

- Author:

- Press Office

- Link:

- www.woodmac.com/...

- Keywords:

- Wood Mackenzie, offshore, wind energy, global, Europe, investors, data, consortiums, tender, asset, USA, Taiwan, China

All news from Wood Mackenzie Ltd

news in archive

Related News