News Release from Wood Mackenzie Ltd

Wind Industry Profile of

China's renewables boom year poses major challenges to western markets

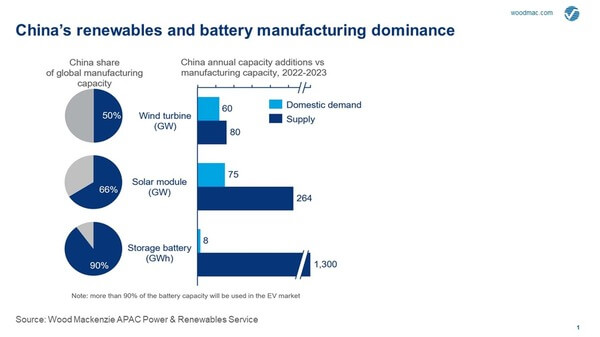

China’s need to meet soaring power demand coupled with ambition to reduce its dependence on coal and gas have given local manufacturers the incentive to grow big. As a result, Wood Mackenzie projects in its latest report Power Play, that China’s production capacity for solar modules is rising faster than forecast global demand, while its wind turbine component and battery manufacturing capacity will grow by 42% and 150%, respectively, over the next two years.

Research director Alex Whitworth said: “This production of epic proportions is enough to meet what China needs to accelerate decarbonisation while supporting the ambitions of much of the rest of the world.”

China’s position as the world’s dominant supplier of solar modules looks secure with nearly 70% of global manufacturing. And while Chinese manufacturers have not quite made such significant inroads into overseas markets for wind turbines, they still account for 50% of global manufacturing, mainly for the domestic market. The country also accounts for nearly 90% of global manufacturing capacity of lithium-ion batteries.

“But this also creates a political headache for many countries that have announced more ambitious 2030 emissions targets on the promise of jobs and prosperity. Achieving this without greater dependence on China looks harder than ever as its manufacturers expand capacity and drive down costs. And with China’s power demand now cooling on the back of more manageable economic growth, local manufacturers are looking to further extend global reach,” Whitworth said.

Principal analyst Xiaoyang Li said: “The sheer scale of its manufacturing capacity affords China a major competitive advantage. Despite increases in raw material prices since 2020, China’s massive expansion in clean energy manufacturing and ability to scale up output has seen its manufacturing costs decrease relative to its global competitors. Chinese wind turbine prices fell by 24% on the year in 2021 and will drop by a further 20% in 2022.”

https://static.windfair.info/uploads/image/imagedata/6134/max_width_wood_mackenzie_20220221_2.jpg

Wood Mackenzie expects equipment costs to retreat in 2023 as commodity prices recede, logistical bottlenecks ease and supply-chain investments are made. China’s renewables capacity investments and rising output will be a key part of this trend, and while the cost of capital for Chinese companies is currently higher than in the US and Europe, interest rates will rise in these markets while they have recently fallen in China. Just as China’s boom year played its part in pushing up clean energy costs for the rest of the world, China’s manufacturers are already helping to drive them down again, further propagating its dominance in energy transition technologies.

However, it is not all sunshine and roses in China. The massive deployment of clean energy is dependent on the availability of a wide range of raw materials, including aluminium, copper, nickel, lithium, cobalt, rare earths, graphite and silicon. China could potentially face supply disruption risks, for example for Australian lithium, as well as China-owned nickel and cobalt production in less stable regions such as the Democratic Republic of Congo. China’s domestic power shortages in 2021 also forced the closure of polysilicon factories in western China, and some solar module plants in Guangdong.

But more importantly, the country is facing increasing anti-China sentiment in western markets and will have to rebuild its brand as a responsible superpower.

To counter this, Chinese clean energy manufacturers are actively investing overseas to avoid both anti-China sentiment and the barriers to market entry that increasingly come with the ‘Made in China’ label. China is also greening its massive Belt and Road Initiative, ending coal-fired plant investment overseas and channelling more capital into renewables made by Chinese companies. The rising cost of financing coal plants, carbon price risks and the growing competitiveness of solar and wind may be the economic drivers, but ditching coal could bring PR success.

Partly in response to China’s dominant position, western markets have introduced policy and taxonomy initiatives designed to put the spotlight on the sustainability and supply chain of clean energy investments and to offer greater support for local manufacturers.

In the US, the current administration has recently extended the Trump-era solar tariffs that have effectively limited Chinese-made solar modules accessing the US market. In addition, President Biden’s climate agenda includes extending solar investment tax credits for another 10 years and allowing the technology to take advantage of the federal production tax credit and direct payment. The same bill also includes a solar manufacturing tax credit that helps lower the cost to produce solar modules in the US and boost domestic supply's competitiveness. If passed by Congress, the tax incentives will more than offset the near-term project cost increase. The EU taxonomy is similarly aimed at helping the bloc scale up sustainable investment and implement the European Green Deal. But competing with China will require more than tax breaks and stricter market-entry regulations.

Li said: “For western markets, there is a rising call for collaboration between governments, miners and energy producers to access raw materials in an equitable and sustainable manner. And for manufacturers, it is the push for greater technical innovation, efficiencies and reliability.”

Continued technological innovation is also critical. A push for lower cost battery alternatives such as lithium iron phosphate battery, for example, could reduce dependence on Chinese producers. By advancing technology, securing access to key resources, driving up efficiency, incentivising investment through effective policy and taxonomy and partnering with Chinese companies, opportunities abound.

Clean energy manufacturers outside of China are also responding, producing larger and more efficient battery units with lower lifetime costs and less outages to compete against their Chinese rivals. And with governments increasingly tying clean energy agendas to investment at home, local supply chains are featuring in tenders for renewables, bringing advantages for manufacturers and project developers supporting domestic employment.

Principal analyst Shirley Zhang said: “While China’s dominance in renewables is clear, its long-term energy transition strategy is arguably flawed by its over-dependence on wind and solar.

“China is far from a global leader in several of the sectors that will be equally critical to reducing emissions, including carbon capture, low-carbon hydrogen, and even further ahead, emerging technologies such as next-generation green fuels. This presents opportunities for those more advanced in these areas to gain competitive advantage and work with China.”

Whitworth said: “For China, the energy transition is a golden opportunity to develop key industries and technologies while improving its green credentials. Accelerating efforts to tackle its own emissions while supporting global decarbonisation sounds like an irresistible proposition.

“For the western economies, responses are more wide-ranging - tariffs, local content policies, tax breaks, collaboration, technical innovation, etc. Competition from all sides is intense, which should bring benefits to the trajectory of global decarbonisation.”

- Source:

- Wood Mackenzie

- Author:

- Press Office

- Link:

- www.woodmac.com/...

- Keywords:

- Wood Mackenzie, China, market, ambiton, manufacturer, challenge, reduction, analysis, capacity, wind power, solar, battery, renewable energy

All news from Wood Mackenzie Ltd

news in archive

Related News

{kind=link}