GB Electricity Market Summary: Second Quarter 2018 April to June

Levels of coal-fired generation remained low in the quarter and for the first time since the early days of the power market a full quarter saw levels of coal-fired generation drop below 1TWh. This meant that coal plants (0.9TWh) only provided a low 1% of the generation in the quarter, with carbon prices remaining high enough for gas-fired plants (28.0TWh) to provide 41% of power, with nuclear plants providing an additional 23% (15.5TWh).

Around 7% of electricity generation was sourced via imports from other power markets (primarily from the continent), with 28% of power being sourced from renewable generators.

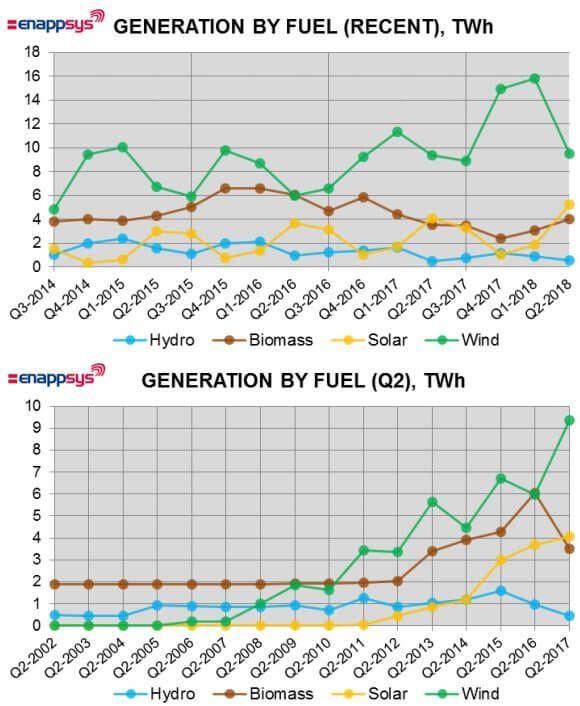

Levels of renewable generation (19.4TWh) continue to climb, but although solar output has frequently been peaking close to 10GW, solar farms continued to provide slightly over a quarter of the total renewable generation.

The achieved levels of renewable generation were not only a significant increase from the levels noted in Q2 2017 (an increase of 11%), but also marked a new high; with Q2 2017 having been the previous highest total for a second quarter.

Wind farms continued to provide almost half of the renewable generation throughout the quarter, with a large increase in wind output levels following the addition of a number of large offshore wind farms in recent quarters.

Overall solar farms provided almost 8% of the total generation in the quarter, but for this to match the peak ~20% levels of total generation that wind farms can achieve in winter, the combination of solar and storage in the market will be required. Otherwise it is likely that the growth in solar capacity would result in price cannibalisation during peak midday hours, limiting earnings at solar plants in the market.

By contrast, levels of wind capacity are already high enough to achieve a large share of total generation in the market and whilst these levels dropped back to 15% of total generation during the quarter, this is a seasonal reduction from around 19-20% in the winter months.

Overall 41% of power came from gas-fired plants, 28% from renewables, 23% from nuclear plants, 7% from imports and 1 from coal plants. Of the power that came from renewables, 49% came from wind farms, 27% from solar farms, 21% from biomass and 3% from hydro.

Read the wole report here.

- Source:

- EnAppSys

- Author:

- Press Office

- Link:

- www.enappsys.com/...

- Keywords:

- UK, GB, electricity, solar, wind, coal, prices, electricity generation