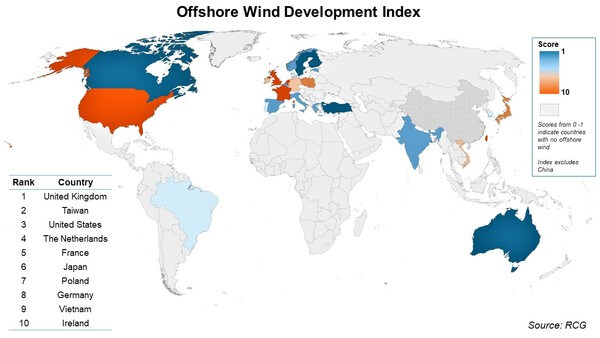

United Kingdom global hotspot for offshore wind development, but potential spread globally

The European market in particular saw a dramatic reduction in electricity prices for offshore wind project contracts in the United Kingdom, France, and the Netherlands. The allocation of 5.5 gigawatts (GW) of offshore wind contracts under the United Kingdom’s third contract for difference (CfD) round at record low prices show that the technology is cost competitive with fossil fuel based generation. The initiation of the fourth round of seabed leasing in 2019 confirmed the United Kingdom’s ambitions to add more offshore wind capacity.

The wider Asian market has experienced significant growth in 2019, covering various stages of offshore wind project development. Taiwan retained its position at second place in RCG’s OSWD Index, with continued progress towards its 2030 offshore wind target. The lowering of feed-in tariff (FiT) prices at the beginning of 2019 struck a balance between encouraging cost reductions whilst still providing a good level of support for new developments. Other markets in the Asia Pacific region made strong progress.

Leasing activity at the federal level in the United States may have stalled in 2019. However the combined efforts of individual states continue to move the industry forward, with the award of substantial power purchase agreements and ambitious new targets set for offshore wind procurement through to 2030.

Top 10 countries according to RCG’s Offshore Wind Development Index (Image: RCG)

A reduction in costs of offshore wind power generation has been driven by technological advances and increasing efficiency in the global supply chain. The introduction of larger turbines has reduced the levelized cost of energy for prospective projects. The floating wind market also continues to see innovation through the installation of new foundation design prototypes.

Overall, RCG’s outlook, from its Global Offshore Wind: Annual Market Report, is that the global market will hit, and maintain, a 6 GW per annum commissioning rate from 2022 onwards at least.

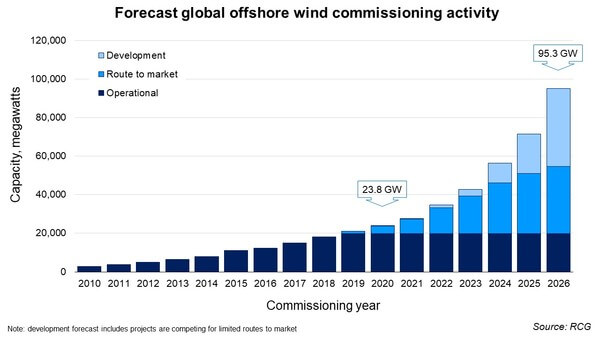

Just under 20 GW of capacity has been brought online by the industry to date. Europe has been the dominant market so far; accounting for 98% of the global commissioned base.

Commissioning activity is expected to fall slightly in 2020 but is expected to rebound to c. 3.5 GW per annum in 2021. RCG sees a significant increase in activity from 2022 onwards, to a rate of over c. 6 GW per annum, driven by projects in the UK, France, Taiwan, USA and the Netherlands.

Offshore wind global commissioning activity and forecast (Image: RCG)

There are five key take-aways from RCG’s latest Global Offshore Wind: Annual Market Report:

1. Average project size continues to increase

There is a strong correlation between the average project size and operational year, with projects in later years seeing much increased installed capacities as the industry matures.

This can be partly attributed to larger lease areas, but developers are also combining projects to deliver economies of scale, maximise operational efficiencies, and reduce environmental impacts.

2. Capital expenditure per megawatt is falling

The trend of increasing reported project CAPEX per MW, driven by projects moving further from shore (and into deeper waters) and growing in scale and size, peaked around the year 2012. The industry is now more adept at controlling and reducing project CAPEX per MW as the industry truly becomes cost effective. This trend aligns with the lower auction prices that are being seen across the world.

3. Asia Pacific markets are challenging Europe

With offshore wind development in Taiwan, Japan, and Vietnam accelerating, financial investment activity in Asia Pacific markets eclipsed Europe for the first time during 2019. Taipei’s offshore wind development plan, supported by a feed in tariff, is starting to bear fruit with five projects reaching financial close in 2019. Investment activity wasn’t confined to Taiwan, with projects in Vietnam and Japan also reaching financial close over the last year. South Korea remains in the mix and key market to watch.

4. Wind turbine order book robust

The number of offshore turbines on order is approaching the number of units installed in the water (around 5,000), reflecting the projected rapid growth in installed capacity over the coming years. Despite the trend for larger turbines, the increased capacity of projects has offset the potential reduction in the number of individual units on order. Further innovations on the horizon, including floating turbines, will open up new resources and markets.

5. United States development pipeline strong

Commissioning activity in the United States is expected to pick up from 2022 onwards, when the first commercial scale projects are due to come online. Over 6 GW of offtake has already been secured, providing a strong route to market, but RCG analysis shows that there is more to come.

Commenting on the Global Offshore Wind: Annual Market Report, RCG’s COO, Dr Lee Clarke said: “There is an unprecedented and rapid transition underway in the energy system, requiring trillions of dollars of investment. Offshore wind power is continuing to establish itself as a cost-effective alternative to fossil fuel based energy sources. RCG’s Offshore Wind Development Index provides an effective barometer of global hotspots for new offshore wind asset development. The latest rankings, published in our Annual Market Report, which contains a host of other data, reflect the fact that certain markets are maturing, whilst others power ahead.” – Lee Clarke, COO, RCG.

Offshore Wind Development Index rankings (Image: RCG)

China has huge potential to become a market leader, but is very well known for its commercial privacy across all industry sectors. Obtaining accurate information regarding its developments is very challenging and for that reason, China is included in RCG’s Annual Market Report, but is excluded from the global hotspot analysis for 2019.

RCG’s full analysis and forecasts can be viewed in its Global Offshore Wind: Annual Market Report. The 131-page piece of work includes details on each offshore wind market with analysis of the resources that will allow projects to reach route to market, financial close, and commissioning milestones. It contains over 150 detailed charts, 45 tables and numerous maps. An overview of the global supply chain is also provided for various aspects of the wind farm engineering procurement construction installation (EPCI) process, as well as a breakdown on all development activity for each offshore wind market in 2019.

To purchase a copy of the Annual Market Report, click HERE

- Source:

- Renewables Consulting Group

- Author:

- Press Office

- Link:

- thinkrcg.com/...

- Keywords:

- RCG, offshore, UK, wind farm, wind energy, asset development, development, index, published, market, annual market, investment