News Release from windfair.net

Wind Industry Profile of

Global: New study says coal and gas stay cheap, but renewables still win race on costs

Low prices for coal and gas are likely to persist, but will fail to prevent a fundamental transformation of the world electricity system over coming decades towards renewable sources such as wind and solar, and towards balancing options such as batteries.

The latest long-term forecast from Bloomberg New Energy Finance, entitled New Energy Outlook 2016, charts a significantly lower track for global coal, gas and oil prices than did the equivalent projection a year ago. Crucially, however, it also shows a steeper decline for wind and solar costs.

The forecast, covering the 2016-40 period, has mixed news on carbon emissions. Weaker GDP growth in China and a rebalancing of its economy will mean emissions there peak as early as 2025. However, rising coal-fired generation in India and other Asian emerging markets indicate that the global emissions figure in 2040 will still be some 700 megatonnes, or 5%, above 2015 levels.

Seb Henbest, head of Europe, Middle East and Africa for BNEF, and lead author of NEO 2016, commented: “Some $7.8 trillion will be invested globally in renewables between 2016 and 2040, two thirds of the investment in all power generating capacity, but it would require trillions more to bring world emissions onto a track compatible with the United Nations 2°C climate target.”

Here are 10 of the eye-catching findings from NEO 2016:

- Coal and gas prices to stay low. Bloomberg New Energy Finance has reduced its long-term forecasts for coal and gas prices by 33% and 30% respectively, reflecting a projected supply glut for both commodities. This cuts the cost of generating power by burning coal or gas.

- Wind and solar costs fall sharply. The levelised costs of generation per MWh for onshore wind will fall 41% by 2040, and solar photovoltaics by 60%, making these two technologies the cheapest ways of producing electricity in many countries during the 2020s and in most of the world in the 2030s.

- Fossil fuel power attracts $2.1 trillion. Investment in coal and gas generation will continue, predominantly in emerging economies. Some $1.2 trillion will go into new coal-burning capacity, and $892 billion into new gas-fired plants.

- But renewables take lion’s share. Some $7.8 trillion will be invested in green power, with onshore and offshore wind attracting $3.1 trillion, utility-scale, rooftop and other small-scale solar $3.4 trillion, and hydro-electric $911 billion.

- The 2?C scenario would require much more money. On top of the $7.8 trillion, the world would need to invest another $5.3 trillion in zero-carbon power by 2040 to prevent CO2 in the atmosphere rising above the Intergovernmental Panel on Climate Change’s ‘safe’ limit of 450 parts per million.

- Electric car boom supports electricity demand. EVs will add 2,701TWh, or 8%, to global electricity demand in 2040 – reflecting BNEF’s forecast that they will represent 35% of worldwide new light-duty vehicle sales in that year, equivalent to 41m cars, some 90 times the 2015 figure.

- Small-scale battery storage, a $250bn market. The rise of EVs will drive down the cost of lithium-ion batteries, making them increasingly attractive to be deployed alongside residential and commercial solar systems. We expect total behind-the-meter energy storage to rise dramatically from around 400MWh in today to nearly 760GWh in 2040. We expect total behind-the-meter energy storage to rise dramatically from around 400MWh in today to nearly 760GWh in 2040.

- China coal-fired generation will follow weaker trend than previously projected. Changes in the Chinese economy, and a move to renewables, mean that coal-fired generation there in 10 years’ time will be 1,000TWh, or 21% below, the figure predicted in BNEF in last year’s NEO.

- That makes India the key to the future global emissions trend. Its electricity demand is forecast to grow 3.8 times between 2016 and 2040. Despite investing $611bn in renewables in the next 24 years, and $115 billion in nuclear, it will continue to rely heavily on coal power stations to meet rising demand. This is forecast to result in a trebling of its annual power sector emissions by 2040.

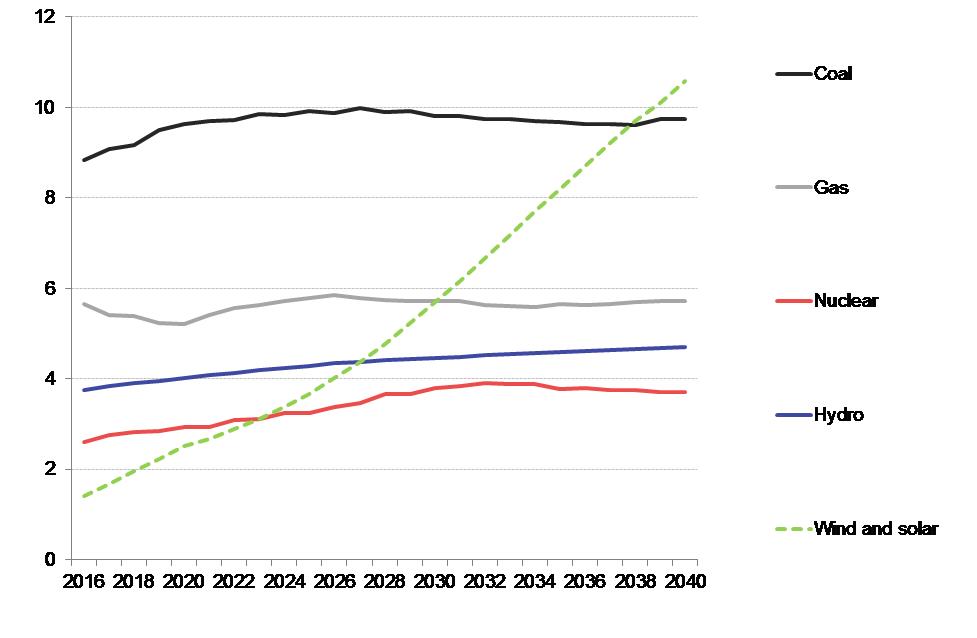

- Renewables to dominate in Europe, to overtake gas in the US. Wind, solar, hydro and other renewable energy plants will generate 70% of Europe’s power in 2040, up from 32% in 2015. In the US, their share will jump from 14% in 2015 to 44% in 2040, as that from gas slips from 33% to 31%.

Jon Moore, chief executive of Bloomberg New Energy Finance, said: “The New Energy Outlook incorporates a significantly lower trajectory for coal and gas prices than the 2015 edition did a year ago but, strikingly, still shows rapid transition towards clean power over the next 25 years.”

Elena Giannakopoulou, senior energy economist on the NEO 2016 project, added: “One conclusion that may surprise is that our forecast shows no golden age for gas, except in North America. As a global generation source, gas will be overtaken by renewables in 2027. It will be 2037 before renewables overtake coal.”

Annual electricity output by the major generating technologies, 2016-40, thousand TWh

Source: Bloomberg New Energy Finance NEO 2016

The outlook for coal is crucial for international ambitions on climate. The Paris conference last December saw 196 nations agree limit global warming to “well below” two degrees Centigrade, and to aim to reach “global peaking of emissions as soon as possible”. NEO 2016 indicates that, despite the global move towards renewables, power sector emissions will not peak for another 11 years.

NEO 2016 is based on a combination of the project pipeline in each country, current policies, plus modelled paths for future electricity demand, power system dynamics and technology costs. It does not assume any further policy measures post-2020, to speed up decarbonisation. Some 65 specialist analysts worked on the forecast.

- Source:

- Bloomberg New Energy Finance

- Link:

- www.bnef.com/...